Univariate time series forecasting without LSTM#

This tutorial example presents how to perform forecasts for an univariate time series while using a simple fourrier-form periodic component rather than a LSTM neural network.

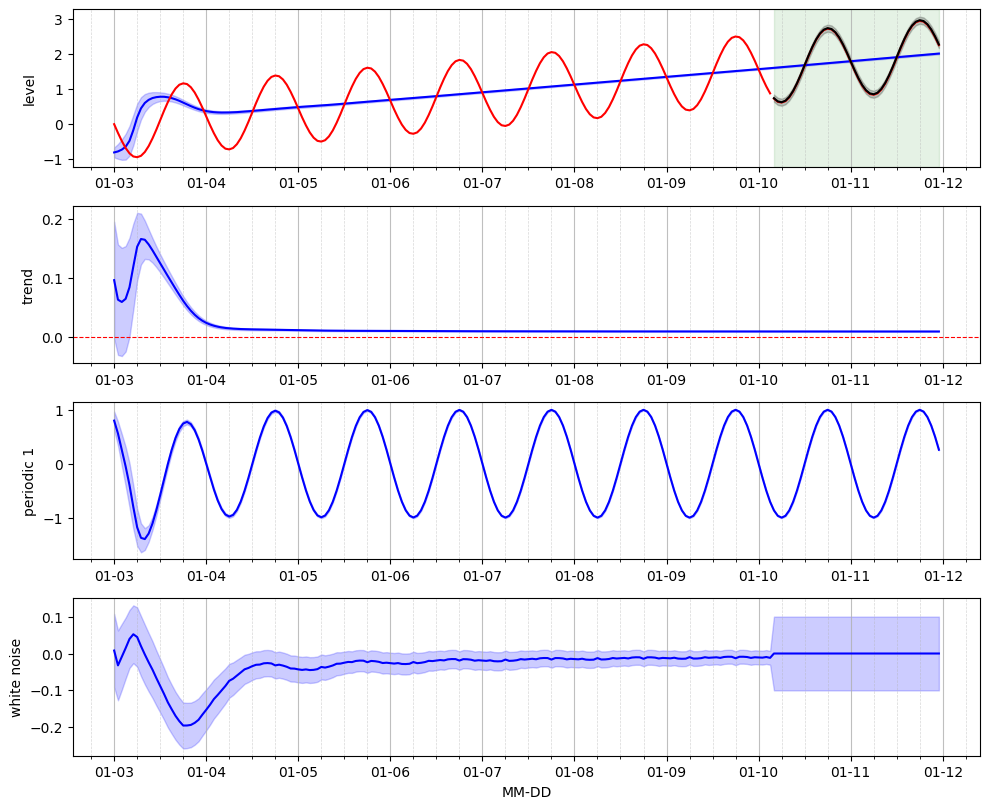

In this example, we use a simple sine-like signal onto which we added a synthetic linear trend.

Import libraries#

Import the various libraries that will be employed in this example.

[1]:

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from pathlib import Path

Import from Canari#

From Canari, we need to import several classes that will be reused in this example. Notably, we need to import the components that will be used to build the model; In terms of baseline, we use the LocalTrend and components. The recurrent pattern is modelled using a Periodic component, and the residual is modelled by a WhiteNoise compoment.

[2]:

from canari import (

DataProcess,

Model,

plot_data,

plot_prediction,

plot_states,

)

from canari.component import LocalTrend, Periodic, WhiteNoise

Read data#

The raw .csv data is saved in a dataframe using the Panda external library.

[3]:

project_root = Path.cwd().resolve().parents[1]

data_file = str(project_root / "data/toy_time_series/sine.csv")

df = pd.read_csv(data_file, skiprows=1, delimiter=",", header=None)

# Add a trend to the data

linear_space = np.linspace(0, 2, num=len(df))

df = df.add(linear_space, axis=0)

#

data_file_time = str(project_root / "data/toy_time_series/sine_datetime.csv")

time_index = pd.read_csv(data_file_time, skiprows=1, delimiter=",", header=None)

time_index = pd.to_datetime(time_index[0])

df.index = time_index

df.index.name = "time"

df.columns = ["values"]

Data preprocess#

In terms of pre-processsing, we define here our choice of using the first 80% of the raw time series for trainig and the following 20% for the validaiton set.

[4]:

output_col = [0]

data_processor = DataProcess(

data=df,

train_split=0.8,

validation_split=0.2,

output_col=output_col,

standardization=False,

)

train_data, validation_data, test_data, standardized_data = data_processor.get_splits()

data_processor.data.head()

[4]:

| values | |

|---|---|

| time | |

| 2000-01-03 00:00:00 | 0.000000 |

| 2000-01-03 01:00:00 | -0.250698 |

| 2000-01-03 02:00:00 | -0.481395 |

| 2000-01-03 03:00:00 | -0.682093 |

| 2000-01-03 04:00:00 | -0.832791 |

Define model from components#

We instantiatiate each component brom the corresponding class. The local_trend baseline component relies on the default hyperparameters. The recurrent pattern will use Fourrier-form Periodic component. The residual is modelled by a Gaussian white noise with a mean 0 and a user-defined standard deviation of 0.1.

Note that we use auto_initialize_baseline_states in order to automatically initialize the baseline hidden states based on the first day of data.

[5]:

local_trend = LocalTrend()

pattern = Periodic(mu_states=[0,0],var_states=[1,1],period=24)

residual = WhiteNoise(std_error=0.1)

model = Model(local_trend, pattern, residual)

model.auto_initialize_baseline_states(train_data["y"][0 : 24])

Filter on train data#

We perform recursive SSM 1-step ahead prediction- and update-steps using the Kalman filter over the entire training set.

[6]:

mu_train_pred, std_train_pred, states=model.filter(data=train_data)

Forecast on validation data#

We perform recursive 1-step ahead forecasts on the validatiobn set.

[7]:

mu_val_pred, std_val_pred, states=model.forecast(data=validation_data)